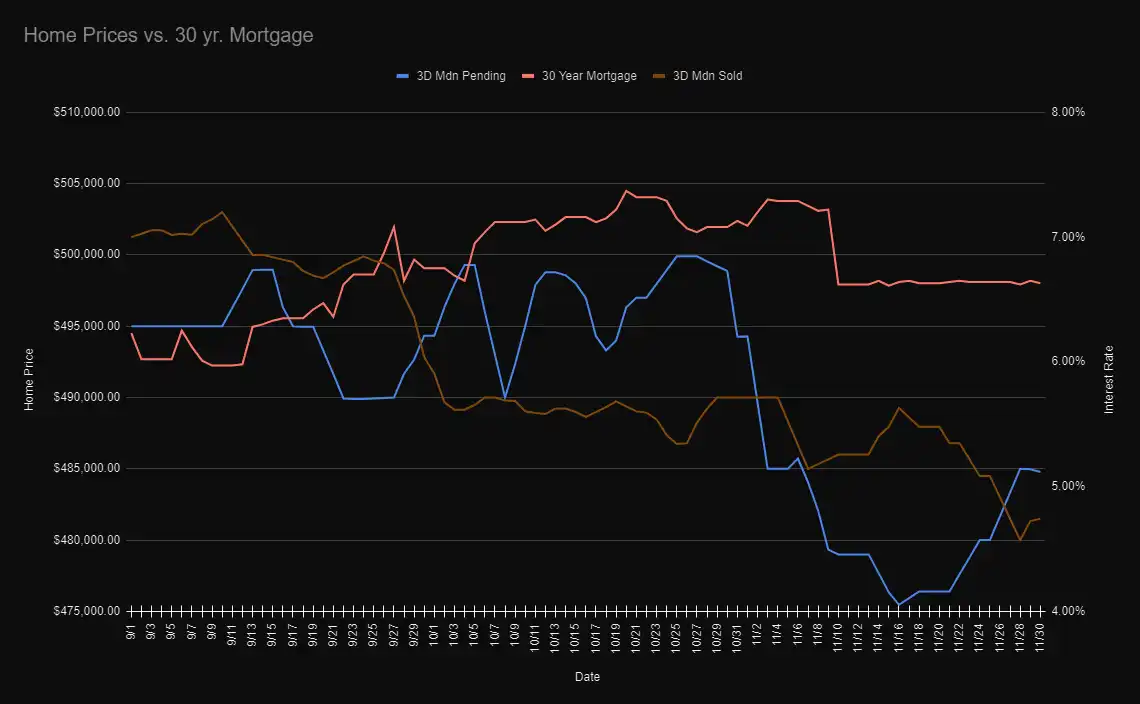

While October proved to be quite uncertain in terms of median home price action, November was anything but that. Utah’s home prices were slapped down 2% over the course of the month, even with MBSs (Mortgage Backed Securities) and interest rates doing rather well. As October's prices failed to move from September's, this month made up for that causing Utah to retain a 1% decline per month pace. There’s a lot to unpack with that, so let’s jump straight into it.

A brief summary of recent financial news and its effect on interest rates.

- 11/2 – Fed raises rates 0.75. Rates up 7.13 to 7.29

- 11/10 – CPI release, massive instantaneous rally on CPI reading at 0.3 MoM (Month over Month). Biggest rally in over a decade for bonds. Massive interest rate reduction 7.22% to 6.62%

- Flat into the holiday

- 10/30 – Powell speaks. Suggests reducing the size of the fed funds rate increases, but says we are still far from over. Addresses other market concerns. Big rally from 6.63% to 6.29% the following day.

- 12/2 Non-farm payroll and unemployment higher than expected, retracting on some of the gains made over the month, but swiftly recovered the same day. 6.29% to 6.34%.

The Federal Reserve is raising their rate based on market data. Their goal is to suppress the market in order to fight off inflation, of which their target is to reach 2% annually. Every time the fed raises their rate, it means less consumer spending and less business income... ideally, anyway. The recent Non-farm payroll and unemployment data, which was relatively strong, tells a story that is best put into words by Matthew Graham, CEO of Mortgage News Daily: "A strong jobs market ALLOWS the Fed to push rates aggressively higher, but it won't prevent the Fed from slowing the pace of rate hikes if inflation continues to subside. Additionally, the Fed knows it has a certain amount of tightening "in the pipeline." That means it has already hiked rates enough that inflation and the economy should increasingly respond, but that the response is far from immediate." I strongly recommend reading his daily articles if you would like a deeper insight into bonds and interest rates.

To recap Utah's Median Home Sales price action, November started off extremely weak. Sales prices fell 1% almost immediately, but pending sales prices dropped 5% in just fifteen days from peak to trough. This comes after September’s pending sales and sales price divergence that retained itself through October (see graph). Pending prices are an indication of what sales prices will be. We go over this relationship more in depth in last month's article. There was a possibility that home prices could see a temporary rebound with fall’s low-volume volatility if you were counting on pending prices being an indicator of sales price. At the beginning of November, prices committed to a 1% drop, then ran for a swift recovery only to be stomped out of those gains and plus another 1% at the end of the month. Total median home sales price losses sit at 2%, or about $10,000.

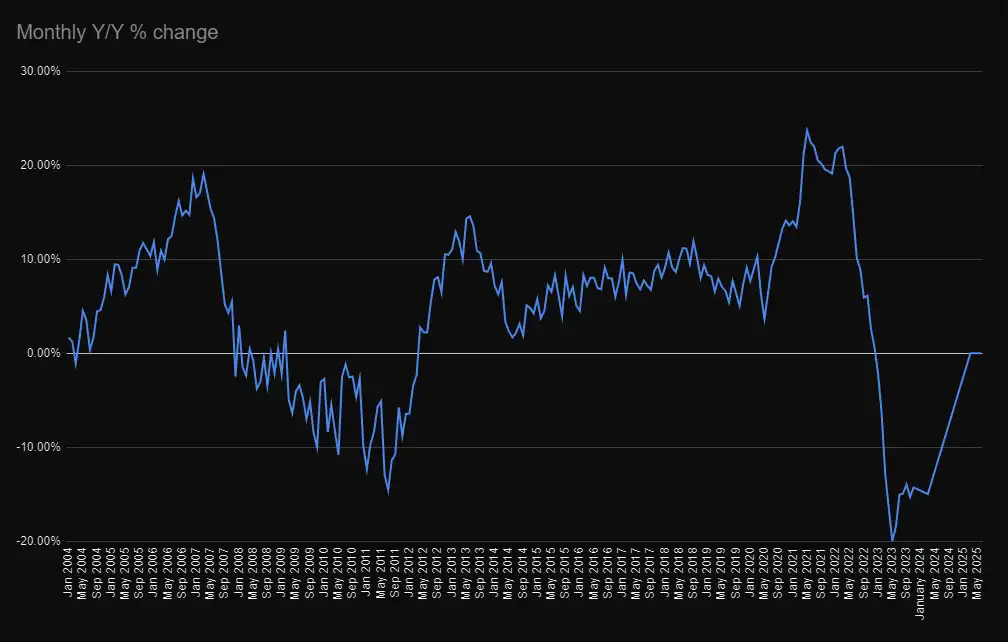

A decline of 2% might seem trivial for just a single month, especially in winter months where declines are expected. However, the sustained decline we’ve experienced over the last few months speaks volumes. From our peak in May, Utah’s home prices have fallen from $540,000 to $480,000 – an 11% decline.

- May – $540,000

- June – $527,000

- July – $506,000

- August – $500,000

- September – $490,000

- October – $490,000

- November – $480,000

If you like to look at Utah’s prices Year over Year, we’ve gone from 19% to 2% from May to November. Retaining a 1% decline per month will put Utah’s year over year at negative 1%, not seen in Utah since March 2012 (the last negative YoY month of the recession).

Assuming a 1% decline per month for one year, we won’t be above water until 2025 and max losses will be around 20%. While we shouldn’t take those numbers as gospel, a simple regression can give us an idea of what happens if we don’t change course. My colleagues and I made a bet on how much the cookie will crumble, and we’re all betting around 15%.

In summary, for interest rates it’s welcomed good news. Having CPI and Powell’s positioning on the Fed Rate is a good start for a changing bond market and interest rates. We now look forward to December’s rate hike, just as likely to be 0.5 rather than 0.75. We will have to see what Jpow and the Fed ultimately decide.

In case you missed last month's article, Click Here